Helped Clients Recover Over $25 Billion. Since 1979.

If you have been injured in a car accident in California, there is a 1 in 6 chance that the other driver was uninsured. And even if they had insurance, there is a high likelihood it was only the minimum coverage — often too low to cover serious injuries or extensive property damage. This is where Uninsured Motorist (UM) and Underinsured Motorist (UIM) coverage step in to protect you.

In this post, we will break down how UM/UIM coverage works, highlight crucial legislative updates, and explain why you need a personal injury lawyer if you’ve been in an accident where the other driver doesn’t have adequate insurance

Uninsured Motorist (UM) coverage pays for your damages when the at-fault driver has no insurance. Underinsured Motorist (UIM) coverage helps when the at-fault driver has some insurance, but not enough to cover your total expenses. Both protect you, the policyholder, when the other party is unable or unwilling to fully pay for your medical bills, lost wages, and pain and suffering.

Most of us carry high amounts of liability insurance — often hundreds of thousands of dollars — to protect ourselves in case we injure someone else in a car crash. This coverage helps pay for the other person’s pain and suffering (general damages), as well as their medical bills, lost income, and property damage (special damages).

But here’s the problem: far too many people stop there.

They forget to protect themselves.

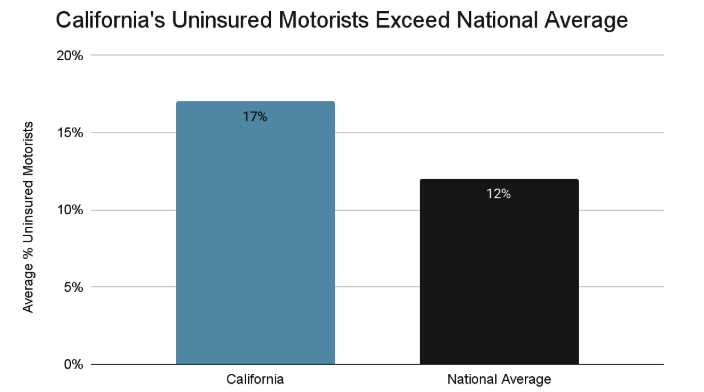

According to the Insurance Research Council, 17% of California drivers have no insurance at all, and many others only carry the minimum legal limits, which won’t come close to covering serious injuries. That means if you are hit by one of these underinsured or uninsured drivers, you could be stuck paying your own medical bills and other expenses — even if the crash wasn’t your fault.

That’s where Uninsured/Underinsured Motorist (UM/UIM) coverage comes in.

Here is something many drivers don’t realize: If you have a solid auto insurance policy — say $250,000 in liability coverage — you’re usually allowed to match that amount with $250,000 in UM/UIM coverage, often for a relatively small increase in premium.

This means you are not just protecting other people in case you cause an accident — you’re also protecting yourself and your family in case someone else hits you and doesn’t have enough insurance.

Example: If you carry $250,000/$500,000 in liability coverage, you can typically buy the same amount in UM/UIM coverage. This ensures you’re just as protected when someone else is at fault as you are when you are.

Many drivers are not aware that starting in January 2025, California’s minimum liability coverage increases to $30,000 per person / $60,000 per accident / $15,000 property damage. While this helps, it may still not be enough for severe injuries or accidents with multiple victims.

Here is why it matters:

Always read your insurance policy! Many policyholders don’t realize they have UIM coverage until they speak with a lawyer.

A personal injury lawyer familiar with UM/UIM coverage can help you:

If you live in San Diego or the surrounding area and you have been injured by an uninsured or underinsured driver, don’t wait to seek legal advice. Call our office for a free consultation — we’ll walk you through your rights step by step.

Example:

| Statistic | Value | Source |

|---|---|---|

| Estimated Percent of uninsured CA drivers | ~17% | Insurance Research Council |

| National average uninsured rate | ~14% | Insurance Research Council |

| Old CA insurance minimum limits (through 2024) | 15/30/5 | California Vehicle Code §16056 |

| New minimum limits (effective Jan. 1, 2025) | 30/60/15 | SB 1107 |

Have questions about uninsured or underinsured motorist coverage in California? Looking for an experienced San Diego personal injury attorney to maximize your compensation? Contact us now for a free consultation. Our team has extensive experience handling insurance disputes, arbitration, and litigation to secure the best outcomes for injured victims.

Disclaimer: The information in this blog post is provided for educational purposes only and does not constitute legal advice. If you need legal assistance, please consult a qualified attorney regarding your specific situation.